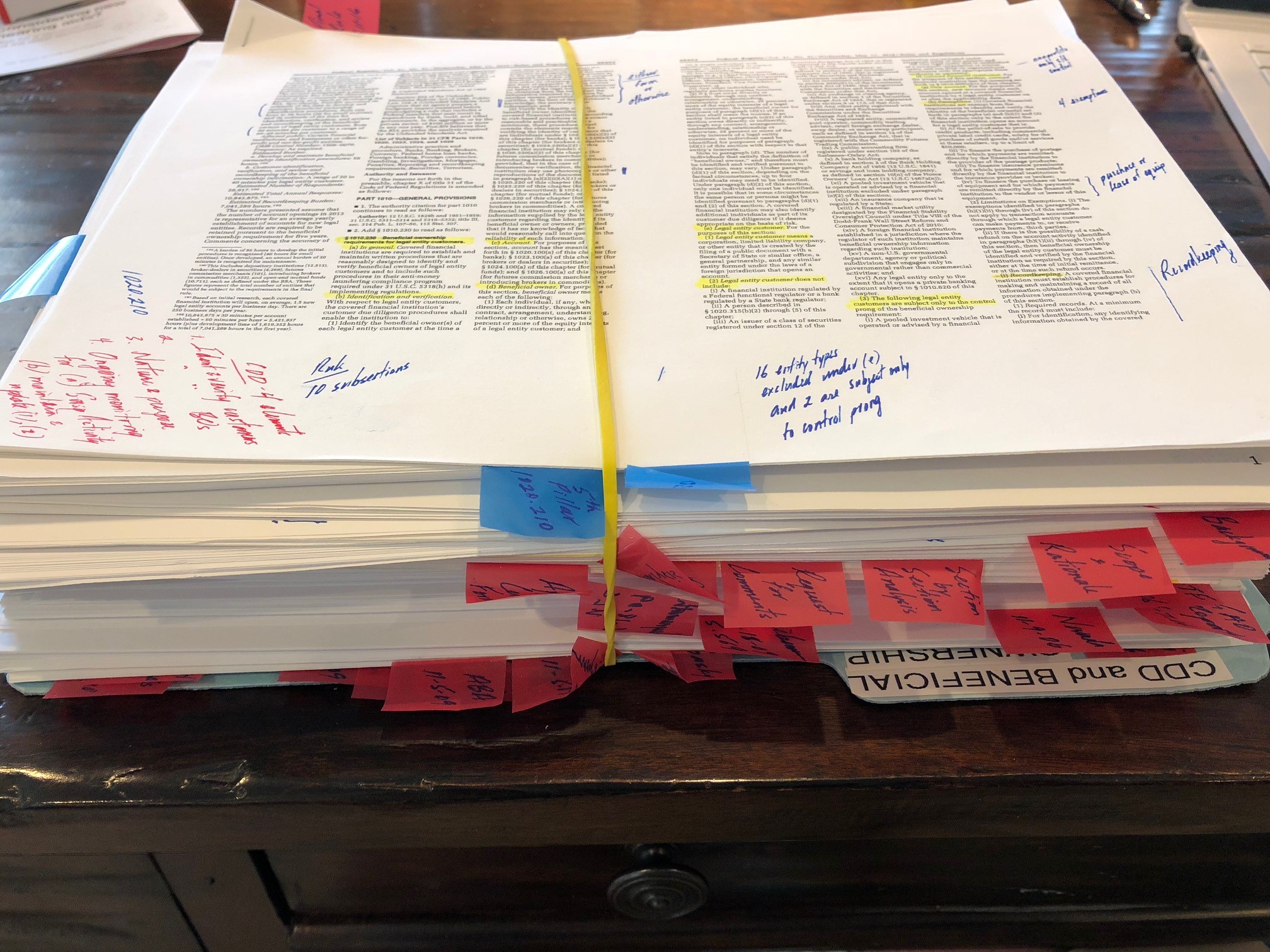

I’m predicting some chaos, lots of gnashing of teeth and wringing of hands, Media and Social Media !WTF?! and Congressional !Calls to Action! as we hit the formal implementation date of May 11th. It’s then (by the way, May 11th is a Friday) that unsuspecting small business owners (and the bookkeepers of those owners) will descend upon confused and unprepared bankers across the country and be asked to fill in a form listing as many as four owners as well as (or) the single person who has effective control of the company (won’t THAT conversation be interesting in some mom-and-pop businesses?).

This requirement has been in the works for more than 20 years – in the mid-1990s there was a call for obtaining beneficial ownership information in the private banking space (Congressional hearings and the New York Fed’s 1997 “Guidance on Sound Practices Governing Private Banking Activities”) and for high risk accounts (such as the 1999 National Money Laundering Strategy that called for a study to provide recommendations to Treasury on “how to assure that [high risk] accounts are traceable to their beneficial interest holders”). We saw beneficial ownership get picked up in the Patriot Act in 2001 (notably the second “Special Measure” in section 311 and for private banking due diligence in section 312), and we saw the U.S. get buffeted in its 2006 FATF Mutual Evaluation results for failing to meet the requirements of Recommendations 33 and 34. All of which led to the 2012 ANPRM, the 2014 NPRM, and the 2016 Final Rule which gave us until May 11, 2018 to implement a beneficial ownership regime. We’re one month away … it is going to get very interesting … and my notes will get a little thicker:

Next Generation of AML?

There is a lot of media attention around the need for a new way to tackle financial crimes risk management. Apparently the current regime is “broken” (I disagree) or in desperate need of repair (what government-run program isn’t in need of repair?).

- Customer- and account-based transaction monitoring is a thing of the past: relationship-based interaction monitoring and surveillance is the NextGen.

- Single entity SAR filers are a thing of the past: 314(b) associations and joint filings are the NextGen.

- A lot of FinTech companies really want AML to be like classical music, where every note is carefully written, the music is perfectly orchestrated, and it sounds the same time and time again regardless of who plays it … but AML is more like jazz: defining, designing, tuning, and running effective anti-money laundering interaction monitoring and customer surveillance systems is like writing jazz music … the composer/arranger (FinTech) provides the artist (analyst) a foundation to freely improvise (investigate) within established and consistent frameworks, and no two investigations are ever the same.

- The federal government has the tools in its arsenal: it simply needs to use them in more courageous and imaginative ways. Tools such as section 311 Special Measures and 314 Information Sharing are grossly under-utilized.

- CTRs are the biggest resource drain in BSA/AML. Because of regulatory drift, CTRs are de facto SAR-lites … get back to basic CTRs and redeploy the resources used in the ever-expanding aggregation requirements to better SARs.

- And remember the “Clash of the Titles” … the protect-the-financial-system (filing great SARs) requirements of Title 31 (Money & Finance … the BSA) are trumped by the safety and soundness (program hygiene) requirements of Title 12 (Banks & Banking), and financial institutions act defensively because of the punitive measures in Title 18 (Crimes & Criminal Procedure) and Title 50 (War … OFAC’s statutes and regulations). There is a need to harmonize the Four Titles and how financial institutions are examined against them. BSA/AML people are judged on whether they avoid bad TARP results (from being Tested, Audited, Regulated, and Prosecuted) rather than being judged on whether they provide actionable, timely intelligence to law enforcement. As the great Hugh MacLeod wrote: “I do the work for free. I get paid to be afraid …”